GST An Understanding and The Way Forward

GST Act - Goods and Service Tax Act is a revolutionary step by the Central Government towards a One Nation, One Tax Indirect Taxation Regime. After a series of Milestones and enormous efforts, deliberations, decisions by the GST Council, GST is finally set for the grand roll out from 1st July 2017. In this article, we attempt to give an overall understanding of what is GST and its important concepts.

GST – MEANING, LEVY AND COLLECTION

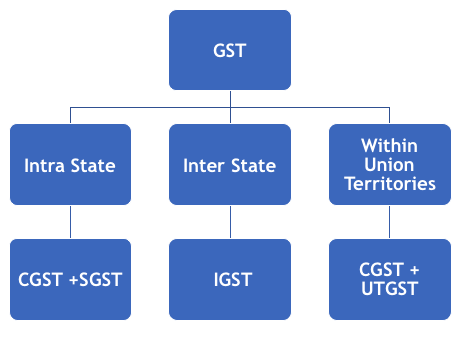

GST is a destination based consumption tax and a comprehensive levy which taxes the SUPPLY of goods and services. The Term Supply has a very wide meaning which includes sale, transfer, barter, exchange, license, rental, lease or disposal made or agreed to be made for a consideration by a person in the course of furtherance of business and also includes import of services. The term supply also includes act of forbearance. GST is a multistage Value Added dual taxation system, where both the Centre and the State have the powers to levy and collect taxes.

Since the powers for levy and collection is with both Centre and the State, GST is classified into CGST (Central Goods and Services Tax), SGST (State Goods and Services Tax), UTGST (Union Territory Goods and Services Tax) and IGST (Integrated Goods and Services Tax). The administrative powers and scenario for charging GST is as follows:

| Particulars | Administered and Levied by |

| CGST | Central Government |

| SGST | State Government |

| UTGST | Central Government |

REGISTRATION

- PAN is a pre-requisite for Registration under GST

- Any Person having an aggregate turnover of more than Rs 20 lakhs across all locations in India wil be required to take registration in the states where supply takes place.

- Aggregate Turnover includes all taxable and non-taxable supplies, exempt supplies and export of goods and or services.

- On Registration, each dealer will be given a unique GSTIN ID.

- Existing registered dealers under VAT, Service Tax, Excise can migrate to GST using the provisional id and upon completion, GSTIN number will be allotted.

INPUT TAX CREDIT

In GST, a registered person is eligible to take Input Credit of CGST, SGST, IGST , UTGST on the supply of goods and or services utilized by him in the course of furtherance of his business.

GST paid on reverse charge basis is also allowed to be taken as input credit.

Input Credit in respect of Capital Goods is allowed to be taken in one instalment.

The Conditions for availing Input Credit are as follows:

- The Registered Person should have received the goods or services.

- He must be in possession of a proper tax invoice for such supply.

- The Supplier should have paid the Taxes on such supply to the Government.

- The Supplier should have filed the returns.

- The Registered Person who is availing the Input Credit should have paid the entire bill amount pertaining to such supply including the GST component to the supplier within 180 days of such supply. In case of failure to pay, the registered person should reverse the Input Credit so availed and is liable for appropriate interest and penalty.

Credits pertaining to IGST/CGST/SGST/UTGST to be accounted separately.

The maximum time limit available for claiming Input Credit for any financial year is the earlier of date of filing the annual return or 20th of October of the next financial year.

INPUT TAX CREDIT NOT AVAILABLE SCENARIOS

a) ITC is not available for motor vehicles and conveyances except when:

- the vehicle is used for the supply of other vehicles or conveyances

- the rule shall not apply if the vehicle is used for transportation of passengers

- the vehicle is used for imparting training on driving, flying, navigating such vehicle or conveyances

No ITC is available for motor vehicles or conveyances used for transportation of goods.

b) No ITC is available for the supply of following goods or services or both:

- food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery except where the category of Inward and outward supply is same or the component belongs to a mixed or composite supply under GST

- sale of membership in a club, health, fitness centre

- ITC would not available for rent-a-cab, health insurance and life insurance except the following

- any services which are made obligatory for an employer to provide its employee by the Indian Government under any current law in force

- where the category is same for the inward supply and outward supply or it is a part of the mixed or composite supply

- in the case of travel, benefits extended to employees on vacation such as leave or home travel concession.

c) ITC shall not be available for any work contract services. ITC for the construction of an immovable property cannot be availed, except where the input service is used for further work contract services.

d) No ITC will be provided for materials used in the construction of immovable property of for furtherance of business. ITC will not be available for the goods or services or both provided to a taxable person used in the construction of an immovable property on his own account including when such goods or services or both are used in the course or furtherance of business.

e) No ITC would be available to the person who has made the payment of tax under composition scheme in GST law.

f) ITC cannot be availed on goods or services or both received by a non-resident taxable person except for any of the goods imported by him.

g) No ITC shall be available for the goods and services or both used for personal consumption and not for business purposes.

h) Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples are not available for claiming ITC under GST.

i) ITC will not be available in the case of any tax paid due to non or short tax payment, excessive refund or ITC utilised or availed by the reason of fraud or willful misstatements or suppression of facts or confiscation and seizure of goods.

MANNER OF UTILISATION OF INPUT CREDITS

| Particulars | Order of Utilisation |

| CGST | CGST IGST |

| SGST/UTGST | SGST/UTGST IGST |

| IGST |

IGST CGST SGST/UTGST |